In a perfect world, your customers would always pay on time, every time. In the real world, things are different. When a business extends payment terms to customers, it often experiences a need for working capital before it receives cash payments on its invoices. By obtaining a small business line of credit through asset-based lending, companies can acquire the capital they need to keep going and growing.

How It Works

Typically, to obtain cash, businesses simply wait for their customers to pay. Unfortunately, without small business lines of credit, many of these companies are held hostage by the very people they serve. Through asset-based financing, companies are able to keep the money flowing in. This helps with cash flow even if invoices are outstanding.

The Asset Based Loan Process

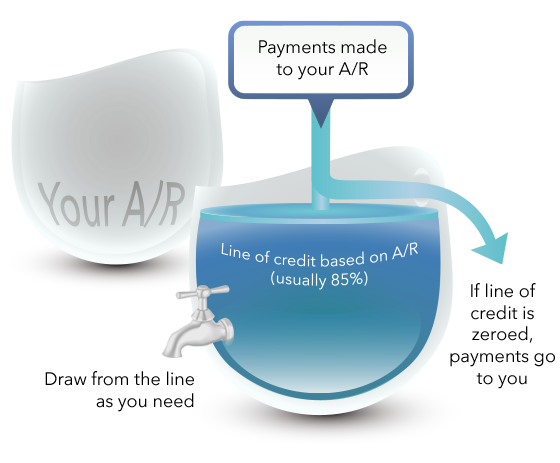

- A Business submits their eligible accounts receivable and A/R aging to Dealstruck

- Dealstruck calculates a “borrowing base” (the total amount of eligible collateral) based on these reports

- Dealstruck advances a line of credit to the business (typically is 80-85% of the borrowing base)

- Payments on the A/R are directed into a bank account managed by Dealstruck (but maintained in the name of the small business) and are used to balance out the line of credit. If it is zeroed the payments are remitted to the business on a weekly basis

- Each week the borrowing base is updated based on new A/R submitted by the business

A commercial line of credit will empower a business to keep functioning while awaiting payments. Asset-based lenders give business owners the opportunity to secure business credit lines that might normally be outside their reach. By applying for a business equity line of credit through Dealstruck’s efficient online platform, you can quickly and easily target an asset-based loan that will meet the needs of your growing small business.